Even if it crashes, Bitcoin may make a dent in the financial world

IN 1999 an 18-year-old called Shawn Fanning changed the music industry for ever. He developed a service, Napster, that allowed individuals to swap music files with one another, instead of buying pricey compact discs from record labels. Lawsuits followed and in July 2001 Napster was shut down. But the idea lives on, in the form of BitTorrent and other peer-to-peer filesharers; the Napster brand is still used by a legal music-downloading service.

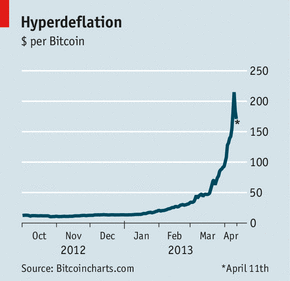

The story of Napster helps to explain the excitement about Bitcoin, a digital currency, that is based on similar technology. In January a unit of Bitcoin cost around $15 (Bitcoins can be broken down to eight decimal places for small transactions). By the time The Economistwent to press on April 11th, it had settled at $179, taking the value of all Bitcoins in circulation to $2 billion. Bitcoin has become one of the world’s hottest investments, a bubble inflated by social media, loose capital in search of the newest new thing and perhaps even by bank depositors unnerved by recent events in Cyprus.

Just like Napster, Bitcoin may crash but leave a lasting legacy. Indeed, the currency experienced a sharp correction on April 10th—at one point losing close to half of its value before recovering sharply (see chart). Yet the price is the least interesting thing about Bitcoin, says Tony Gallippi, founder of BitPay, a firm that processes Bitcoin payments for merchants. More important is the currency’s ability to make e-commerce much easier than it is today.

Bitcoin is not the only digital currency, nor the only successful one. Gamers on Second Life, a virtual world, pay with Linden Dollars; customers of Tencent, a Chinese internet giant, deal in QQ Coins; and Facebook sells “Credits”. What makes Bitcoin different is that, unlike other online (and offline) currencies, it is neither created nor administered by a single authority such as a central bank.

Instead, “monetary policy” is determined by clever algorithms. New Bitcoins have to be “mined”, meaning users can acquire them by having their computers compete to solve complex mathematical problems (the winners get the virtual cash). The coins themselves are simply strings of numbers. They are thus a completely decentralised currency: a sort of digital gold.

Bitcoin’s inventor, Satoshi Nakamoto, is a mysterious hacker (or a group of hackers) who created it in 2009 and disappeared from the internet some time in 2010. The currency’s early adopters have tended to be tech-loving libertarians and gold bugs, determined to break free of government control. The most infamous place where Bitcoin is used is Silk Road, a marketplace hidden in an anonymised part of the web called Tor. Users order goods—typically illegal drugs—and pay with Bitcoins.

Some legal businesses have started to accept Bitcoins. Among them are Reddit, a social-media site, and WordPress, which provides web hosting and software for bloggers. The appeal for merchants is strong. Firms such as BitPay offer spot-price conversion into dollars. Fees are typically far less than those charged by credit-card companies or banks, particularly for orders from abroad. And Bitcoin transactions cannot be reversed, so frauds cannot leave retailers out of pocket.

Yet for Bitcoins to go mainstream much has to happen, says Fred Ehrsam, the co-developer of Coinbase, a Californian Bitcoin exchange and “wallet service”, where users can store their digital fortune. Getting hold of Bitcoins for the first time is difficult. Using them is fiddly. They can be stolen by hackers or just lost, like dollar bills in a washing machine. Several Bitcoin exchanges have suffered thefts and crashes over the past two years.

Ripple effects

As a result, the Bitcoin business has consolidated. The leading exchange is Mt.Gox. Based in Tokyo and run by two Frenchmen, it processes around 80% of Bitcoin-dollar trades. If such a business failed, the currency would be cut off at the knees. In fact, the price hiccup on April 10th was sparked by a software breakdown at Mt.Gox, which panicked many Bitcoin users. The currency’s legal status is unclear, too. On March 18th the Financial Crimes Enforcement Network, an American government agency, proposed to regulate Bitcoin exchanges; this suggests that the agency is unlikely to shut them down.

Technical problems will also have to be overcome, says Mike Hearn, a Bitcoin expert. As more users join the network, the amount of data that has to circulate among them (to verify ownership of each Bitcoin) gets bigger, which slows the system down. Technical fixes could help but they are hard to deploy: all users must upgrade their Bitcoin wallet and mining software. Mr Hearn worries that the currency could grow too fast for its own good.

But the real threat is competition. Bitcoin-boosters like to point out that, unlike fiat money, new Bitcoins cannot be created at whim. That is true, but a new digital currency can be. Alternatives are already in development. Litecoin, a Bitcoin clone, is one. So far it is only used by a tiny hard-core of geeks, but it too has shot up in price of late. Rumour has it that Litecoin will be tradable on Mt.Gox soon.

A less nerdy alternative is Ripple. It will be much easier to use than Bitcoin, says Chris Larsen, a serial entrepreneur from Silicon Valley and co-founder of OpenCoin, the start-up behind Ripple. Transactions are approved (or not) in a few seconds, compared with the ten minutes a typical Bitcoin trade takes to be confirmed. There is no mystery about the origins of Ripple nor (yet) any association with criminal or other dubious activities.

OpenCoin is expected to start handing out Ripples to the public in May. It has created 100 billion, a number it promises never to increase. To give the new currency momentum, OpenCoin plans eventually to give away 75% of the supply. Existing Bitcoin users can already claim free Ripples and eventually anyone opening an OpenCoin account will also receive some.

The 25% retained by OpenCoin will give it a huge incentive to make sure that the Ripple is strong: the higher its value, the bigger the reward for OpenCoin’s investors when the firm cashes out. On April 10th several blue-chip venture-capital firms, including the ultra-hip Andreessen Horowitz, announced that they had invested in OpenCoin.

If Ripple gains traction, even bigger financial players may enter the fray. A firm such as Visa could create its own cheap instant international-payments system, notes BitPay’s Mr Gallippi. And what if a country were to issue algorithmic money?

At that point Bitcoin would probably be bust. But if that happened, its creators would have achieved something like Mr Fanning. Napster and other file-sharing services have forced the music industry to embrace online services such as iTunes or Spotify. Bitcoin’s price may collapse; its users may suddenly switch to another currency. But the chances are that some form of digital money will make a lasting impression on the financial landscape.

Click on the bitcoin logo below to buy, use or accept bitcoin. Unocoin is India’s most popular bitcoin wallet.

To read the bitcoin white paper, visit: https://bitcoin.org/bitcoin.pdf